Here’s a plot from Gemini, not fact checked by me or any other human. Thanks Gemini!

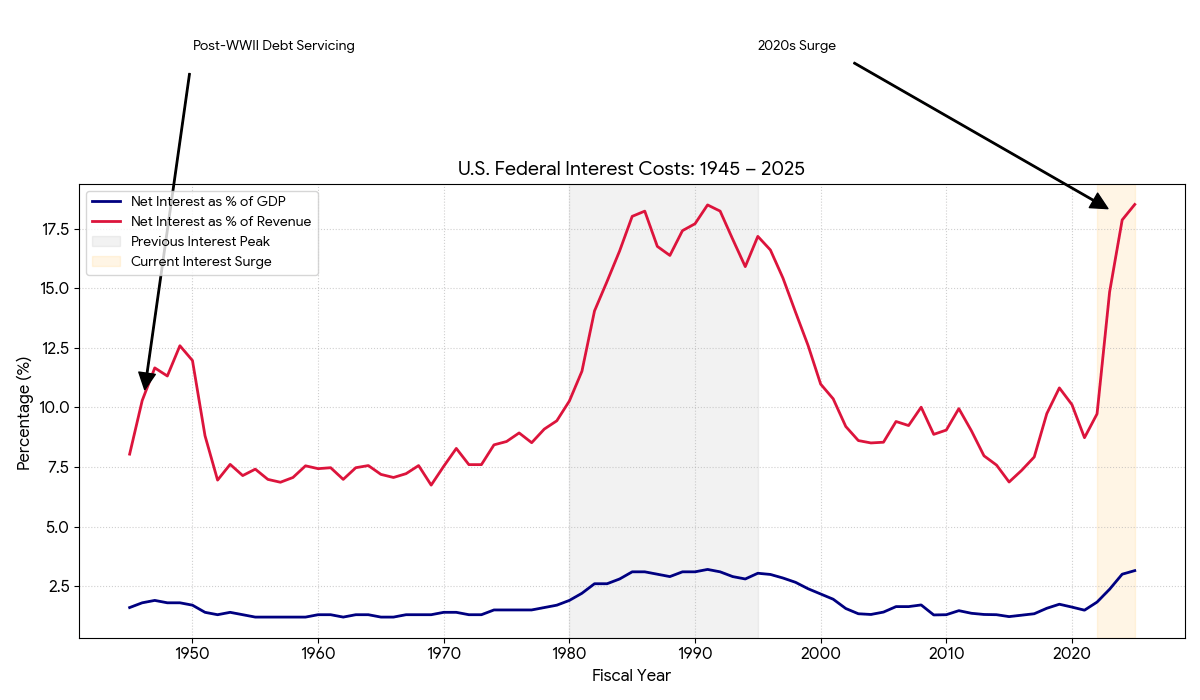

I’ve always thought reporting “debt as % of GDP” is dumb. What really matters is how much interest payments on the debt are relative to the size of our economy. Or, in a more rational, less political environment, that is all that would matter – but in our real world politics matters a lot, and because politics limits our government’s ability to use taxes to pay the debt, debt payments as % of tax revenue also matter.

So…after World War II interest payments on the debt were very high, but this wasn’t a big deal because the economy was growing very quickly. In the 1980s and 1990s, interest payments spiked as interest rates spiked and growth slowed down. Eventually interest rates came down and got us out of that particular pickle. But now, from the plot we can see that current interest payments as a % of GDP are spiking to a similar level to how they did in the 1980s and 1990s. Interest rates are higher than they have been in recent decades, but not crazy high like in the 1980s. The difference really is the size of the debt relative to the economy. We can hope for faster growth to get us out of this one – there is some hope for AI-led productivity gains, but at the same time we have our government shooting itself in the foot by gutting research, development, and education spending, the historical underpinnings of our nation’s growth, while also blowing enormous sums on reckless, illegal wars of aggression with no end in site, and actually reducing taxes on affluent tax payers and corporations. We have inflation and interest rates both seemingly ramping up. So the situation does indeed seem pretty dire. Do I really even have to suggest solutions here? Sure, don’t stand in the way of the AI thing, but also don’t put all our eggs in that basket and do the opposite of all the obviously stoopid policies I just mentioned.